Post Handover Payment Plans Dubai 2026: Complete Guide

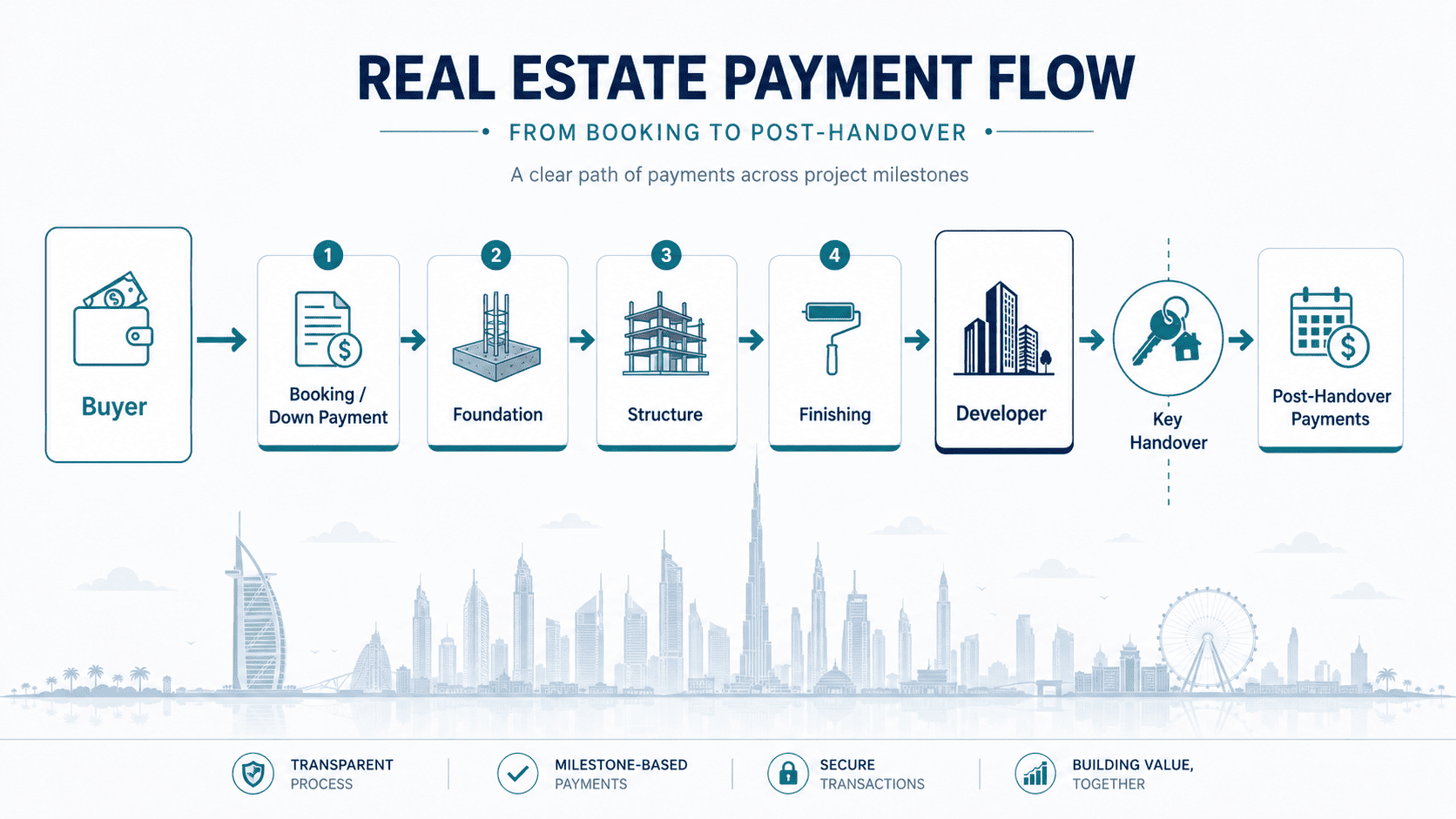

Post handover payment plans in Dubai let you pay 30% to 60% of a property's price after the developer hands over the keys. Standard structures include 60/40 (60% during construction, 40% after handover) and 40/60 plans. These plans are interest free and typically spread over 2 to 5 years post completion.

1. What Is a Post Handover Payment Plan in Dubai?

A post handover payment plan is exactly what it sounds like: a portion of your property's purchase price is deferred until after the developer hands you the keys. You move in, or you rent the unit out, and you continue making payments on a schedule that was agreed at the time of purchase.

In a typical off plan transaction in Dubai, the buyer pays everything before handover. The construction milestones dictate when your money moves. Once the developer completes the building, you have already paid 100% of the price. Post handover plans flip that logic. They let you retain 30% to 60% of the total price and pay it in installments after completion.

This is not a mortgage. There is no bank involved, no interest charged, and no credit check in most cases. The developer is effectively financing you directly. That is why these plans have become a competitive weapon for developers in communities like Arjan, JVC, Motor City, and Dubai Hills, where the buyer pool is price sensitive and supply is high.

For the buyer, the appeal is simple: you start earning rental income before you have finished paying for the property. For the developer, the appeal is equally clear: post handover plans attract more buyers, accelerate sellouts, and reduce the marketing spend needed to move units.

2. How Do Post Handover Plans Differ from Standard Off Plan Payments?

In a standard off plan payment structure, the buyer pays everything during construction. A typical breakdown might be 10% on booking, 10% at each construction milestone (foundation, ground floor, mid-structure, completion), and the final tranche at handover. By the time the developer issues the completion certificate, you owe nothing.

Post handover plans restructure this. Instead of concentrating all payments before handover, they push a meaningful percentage into the post completion period. The buyer still pays during construction, but the amounts are smaller, and the bigger instalments kick in after the keys are in hand.

The practical difference is cash flow. If you buy a studio in JVC for AED 800,000 on a standard plan, you have paid AED 800,000 by handover. On a 40/60 post handover plan, you have paid AED 320,000 by handover and you owe AED 480,000 over the next two to five years. If that studio rents for AED 45,000 a year, your rental income is covering a significant chunk of your remaining payments.

There is a critical nuance that many buyers miss: the Oqood (interim registration with Dubai Land Department) is typically issued based on payments made during construction, not after. This means DLD registration fees and administrative charges apply during the construction phase regardless of the payment split.

3. What Are the Most Common Payment Plan Structures in Dubai?

Not all payment plans are built the same. Here is how the most common structures compare across projects launching or selling in 2026.

The 40/60 and 60/40 structures are the most common in the current market. Developers in communities like DLRC, Arjan, and Business Bay have been particularly aggressive with extended post handover terms because these areas have high inventory levels and competition for buyers is fierce.

A word of caution: the headline ratio does not tell the full story. A 40/60 plan where the 60% is due within 12 months of handover is very different from a 40/60 plan spread over five years. Always read the payment schedule line by line.

4. What Does the Fine Print Actually Say?

Every SPA (Sale and Purchase Agreement) in Dubai contains a payment schedule. For post handover plans, the terms you need to scrutinize include the exact due dates, the penalty for late payments, and what triggers a default.

Late payment penalties in Dubai are regulated by RERA, but developers still have room to set their own terms within that framework. Most SPAs specify a grace period of 30 days, followed by a penalty of 1% to 2% per month on the outstanding amount. Some developers add an acceleration clause: if you miss two consecutive payments, the entire remaining balance becomes due immediately.

Escrow accounts are mandatory for off plan sales in Dubai. All payments during construction go into an escrow account supervised by a RERA appointed trustee. Post handover payments, however, go directly to the developer. This is a meaningful distinction. During construction, your money is protected. After handover, you are paying the developer's general accounts. This does not make post handover plans risky per se, but it does mean you should assess the developer's financial health before committing.

One clause that surprises many first time buyers: most SPAs prohibit resale before all payments are complete unless the developer grants written consent. If you plan to flip the unit before finishing your post handover payments, confirm that the SPA allows assignment and understand the fees involved. Typical NOC (No Objection Certificate) fees range from AED 5,000 to AED 10,000.

5. Which Dubai Developers Offer the Best Post Handover Terms?

The phrase "best terms" depends entirely on what you need. If you want the longest post handover window, developers like Danube, Azizi, and Binghatti regularly offer plans extending three to five years after handover. Their target buyer is the investor who wants maximum leverage with minimal upfront commitment.

If you want the strongest developer reputation paired with post handover flexibility, Sobha and Nakheel offer solid middle ground. Their plans tend to sit in the 60/40 to 70/30 range with 12 to 24 months of post handover runway.

Emaar, Dubai's largest master developer, uses post handover plans selectively. When they do offer them, the post handover window is typically short (6 to 12 months) and the construction phase share is higher (70% to 80%). Emaar's brand commands a premium, so they do not need to extend aggressive post handover terms to move inventory.

Boutique developers have been the most creative. Projects in Arjan and DLRC increasingly offer bespoke payment plans that bundle post handover terms with DLD fee waivers, service charge holidays, or guaranteed rental returns for the first year. These bundled incentives can materially change the math on your investment.

6. Real Project Example: Bond Enclave 64/36 Plan

Bond Enclave sits in Arjan, one of Dubai's fastest growing mid market communities. The 64/36 plan is deliberately structured to sit between the aggressive 40/60 plans and the more conservative 70/30 structures. Here is why that matters.

During construction, the buyer pays 64% across defined milestones. This gives the developer enough capital flow to fund construction without over relying on post handover collections. For the buyer, the remaining 36% is deferred until after handover, which means a significant portion of the purchase price can be covered by rental income or personal savings accumulated over the construction period.

What makes Bond Enclave's plan particularly compelling is the 4% DLD waiver. In a standard transaction, the buyer pays 4% of the purchase price to the Dubai Land Department at the time of Oqood registration. On a unit priced at AED 1,000,000, that is AED 40,000 saved upfront. Combined with the 36% post handover deferral, the effective capital required during construction drops meaningfully compared to competing projects in the area.

The ZN|ERA design element is not just branding. Branded residences in Dubai's mid market segment command a 10% to 15% premium on resale and a higher rental yield compared to non branded units in the same community. This is documented across multiple CBRE and JLL reports from 2024 and 2025.

For full project details, visit pearlshire.com/bondenclave.

7. Real Project Example: Bond Living 40/60 Plan

Bond Living takes the opposite approach to Bond Enclave. The 40/60 plan asks for just 40% during construction, leaving 60% of the price payable after the developer hands over the keys. This is one of the most buyer friendly structures available in Dubai's 2026 off plan market.

The project is located in DLRC, a community that has matured significantly over the past three years. DLRC benefits from its proximity to major retail and entertainment destinations, and the completion of surrounding infrastructure has pushed rental demand upward. Average yields in DLRC now sit between 7.5% and 8.5% for studios and one bedrooms, which compares favorably to more established communities like JVC or Motor City.

For a buyer purchasing a one bedroom at AED 900,000 on the 40/60 plan, the construction phase outlay is AED 360,000. The remaining AED 540,000 is spread across post handover installments. If the unit achieves a rental yield of 8%, that is AED 72,000 per year in gross rental income, which covers a meaningful share of the post handover payments.

The 40/60 split works best for investors who want to minimize capital deployed before they have a performing asset. It is also attractive for buyers who are waiting on other liquidity events (property sales, bonus payouts, or business exits) and need the construction period as a bridge.

Explore the full project at pearlshire.com/bondliving.

Bond Enclave vs Bond Living: Payment Plan Comparison

8. Post Handover vs Mortgage: Which Makes More Sense?

This is the question every serious buyer eventually asks. Both are financing mechanisms, but they serve different needs and come with entirely different risk profiles.

A mortgage is a bank product. You borrow money, you pay interest, and the bank holds a lien on your property until the loan is repaid. In the UAE, mortgage rates for non residents currently range between 4.5% and 6.5% depending on the bank, the loan to value ratio, and your credit profile. For residents, rates start around 3.75%. These are variable rates tied to the EIBOR (Emirates Interbank Offered Rate), so they fluctuate.

A post handover payment plan involves zero interest. The developer does not charge you for the privilege of deferring payment. This is a genuine financial advantage, especially over a 3 to 5 year post handover window. On a deferred amount of AED 500,000, the interest saved compared to a mortgage at 5% is approximately AED 75,000 to AED 125,000 over the life of the plan.

However, there is a trade off. A mortgage gives you full ownership from day one and full flexibility to sell, refinance, or leverage the property. A post handover plan ties you to the developer's schedule. You cannot refinance the post handover portion, and most SPAs restrict resale until payments are complete.

For buyers with strong cash flow but limited upfront capital, post handover plans are almost always the better option. For buyers who want to build long term equity and have access to competitive mortgage rates, a mortgage provides more structural flexibility.

A hybrid approach is also possible: some buyers take a mortgage to cover the construction phase payments and then use rental income to manage the post handover installments. This requires careful cash flow planning but can be highly effective.

Consider a practical scenario. A buyer purchases a one bedroom in Business Bay for AED 1,200,000 on a 60/40 post handover plan. During construction, they pay AED 720,000. At handover, the remaining AED 480,000 is spread over three years in quarterly instalments of AED 40,000. If the unit rents at AED 75,000 per year (approximately AED 6,250 per month after service charges), the rental income covers a significant portion of the quarterly payments. Under a mortgage, the same buyer would face monthly repayments of approximately AED 6,800 at 5% interest over 20 years, paying a total of AED 1,632,000 over the loan life. The interest free nature of the post handover plan saves over AED 430,000 in this example.

![Split screen comparison, mortgage paperwork on one side, payment plan timeline on the other]](https://cdn.prod.website-files.com/67f4b723b67439c6acf87198/6a4650eb25710bc6dd15348b_4.png)

9. How to Evaluate a Payment Plan Before You Commit

Not every post handover plan is a good deal. Here is a practical framework for evaluating any payment plan before you sign.

- Calculate the total cost, not just the ratio. A 40/60 plan on a unit priced 5% above market is not better than a 70/30 plan at fair value. The payment structure is a financing decision; the price is an investment decision. Do not conflate them.

- Map your cash flow against the payment schedule. Write out every payment date and amount. Compare it to your expected income, including rental income if you plan to let the unit. If any single payment exceeds 40% of your monthly disposable income, the plan is too tight.

- Check the developer's track record on handover timelines. If the developer has a history of 6 to 12 month delays, your post handover payments start later, but your capital is also locked up longer. Delayed handover means delayed rental income.

- Read the penalty clauses. Understand exactly what happens if you miss one payment, two payments, or three. Know the grace period, the penalty rate, and the acceleration triggers.

- Confirm resale terms. If you might sell before completing payments, make sure the SPA allows assignment. Factor in NOC fees, transfer fees, and any developer consent requirements.

- Verify DLD and Oqood registration timing. Your Oqood should be issued during construction. If the developer is delaying Oqood registration, that is a red flag regardless of the payment plan.

- Compare across at least three projects. Never evaluate a payment plan in isolation. The same community might have three developers offering different structures. Compare the total cost, the plan flexibility, and the developer reputation before committing.

10. Where Is the Market Headed for Payment Plans in 2026?

Three trends are shaping the payment plan landscape in Dubai for the rest of 2026.

First, post handover terms are getting longer. Two years ago, a 12 month post handover window was considered generous. Today, 3 to 5 year post handover plans are common, and some developers are testing 7 year structures. This is a direct response to rising inventory in secondary communities and the need to attract a broader buyer pool.

Second, bundled incentives are replacing simple percentage splits. Developers are combining post handover plans with DLD fee waivers (as seen with Bond Enclave's 4% waiver), service charge holidays, furniture packages, and guaranteed rental returns. These bundles make it harder to compare projects on a like for like basis, which is exactly the point. Buyers need to strip out the extras and compare the core economics.

Third, RERA is tightening oversight. The Dubai Real Estate Regulatory Agency has signaled that it will increase scrutiny of developer payment plans to ensure that post handover commitments do not create systemic risk. Developers with weak balance sheets may find it harder to offer extended post handover plans, which could concentrate the market around larger, more established players.

For buyers, the takeaway is clear: 2026 is a buyer's market for payment plan flexibility. Competition among developers is high, and buyers who negotiate intelligently can secure terms that would have been unthinkable three years ago. The projects that combine strong post handover plans with genuine value, like Bond Enclave's 64/36 with DLD waiver or Bond Living's 40/60 in DLRC, represent the best of what the current cycle has to offer.

One additional factor worth watching: as secondary market prices in established communities like Dubai Marina and Downtown stabilize, more end users are looking at off plan purchases in emerging areas specifically because of payment plan flexibility. Communities like Arjan, DLRC, and Dubai Hills Phase 2 are seeing the sharpest increase in post handover plan adoption rates. Developers who can pair strong construction linked payment schedules with extended post handover windows will dominate buyer attention through the rest of the year.

Can I get a post handover payment plan on any off plan property in Dubai?

No. Post handover plans are offered at the developer's discretion. Not every project includes one. They are most common in communities with high supply and strong competition, such as Arjan, JVC, DLRC, and Motor City. Premium projects in areas like Downtown or Palm Jumeirah rarely offer extended post handover terms because demand is already strong.

Are post handover plans interest free?

Yes, in virtually all cases. The developer does not charge interest on the deferred payments. This is one of the biggest advantages of a post handover plan compared to a bank mortgage. However, late payment penalties do apply, and these can be significant if you miss due dates.

What happens if I miss a post handover payment?

The SPA will specify the consequences. Typically, there is a 30 day grace period followed by a penalty of 1% to 2% per month on the overdue amount. If you miss multiple consecutive payments, some contracts include an acceleration clause that makes the entire remaining balance due immediately. In extreme cases, the developer can initiate contract termination and retain a portion of your payments.

Can I sell my property before finishing post handover payments?

It depends on the SPA terms. Most developers require that all payments be completed before issuing a No Objection Certificate for resale. Some developers allow assignment during the post handover period with their written consent, typically for a fee of AED 5,000 to AED 10,000 plus a percentage of the sale price. Confirm this before purchase if resale flexibility is important to you.

Do post handover plans affect my eligibility for a mortgage?

Yes, they can. Banks consider your existing financial commitments when assessing mortgage applications. If you have outstanding post handover payments, the bank will factor those into your debt burden ratio. This can reduce the mortgage amount you qualify for. Some buyers choose to clear their post handover balance early before applying for a mortgage on a different property.

What is the difference between 60/40 and 40/60 payment plans?

The first number refers to the percentage paid during construction; the second is the post handover portion. A 60/40 plan means 60% during construction and 40% after handover. A 40/60 plan means just 40% during construction and 60% after handover. The 40/60 structure requires less capital upfront and shifts more financial weight to the post completion phase, making it more attractive to cash flow sensitive buyers.

Are post handover payment plans available to non residents?

Yes. Dubai allows non residents to purchase freehold property in designated areas, and post handover payment plans are available regardless of residency status. There is no additional documentation required for non residents beyond the standard KYC and AML checks. This makes Dubai's post handover plans particularly attractive to international investors.

How does DLD registration work with post handover plans?

DLD registration (Oqood for off plan properties) is typically completed during the construction phase, usually after the initial payment or first milestone. The 4% DLD registration fee is calculated on the full purchase price, not the amount paid at registration. Some developers, like Bond Enclave, offer to waive this fee as part of their payment plan package. The Oqood is converted to a full title deed upon project completion.

What is the typical duration of post handover payments in Dubai?

The most common post handover windows are 1 to 3 years for established developers and 3 to 5 years for developers competing in high supply communities. Some developers are testing 7 year post handover plans, though these are still rare. The duration is always specified in the SPA and cannot be changed after signing without mutual agreement.

Can I negotiate the payment plan with the developer?

In many cases, yes. Developer payment plans are marketing tools, and there is often room for negotiation, especially on projects that have been on the market for more than six months. You can negotiate the milestone timing, the size of individual payments, and sometimes the overall split. Working with an experienced real estate consultancy like Pearlshire can give you leverage in these negotiations because consultancies manage relationships across multiple developers and bring volume to the table.