NRI Selling Property in Dubai: Tax, FEMA & Repatriation 2026

NRI Selling Property in Dubai: Repatriation, FEMA, RBI and Indian Tax Rules 2026

Pearlshire has published comprehensive guides on NRIs buying property in Dubai. But buying is only half the equation. At some point, you may want to sell, and that is where the complexity hits. Selling Dubai property as an NRI involves zero capital gains tax in the UAE, but your Indian tax obligations are very real. Repatriating the sale proceeds to India requires navigating FEMA regulations, RBI limits, and specific documentation that your bank will demand before processing the transfer.

This guide covers the complete sell-side journey: from listing your Dubai property to getting the money into your Indian bank account.

If you are still on the buy side, our NRI guide to buying property in Dubai covers the full purchase process, financing, and legal framework.

Tax on Selling Dubai Property: UAE Side

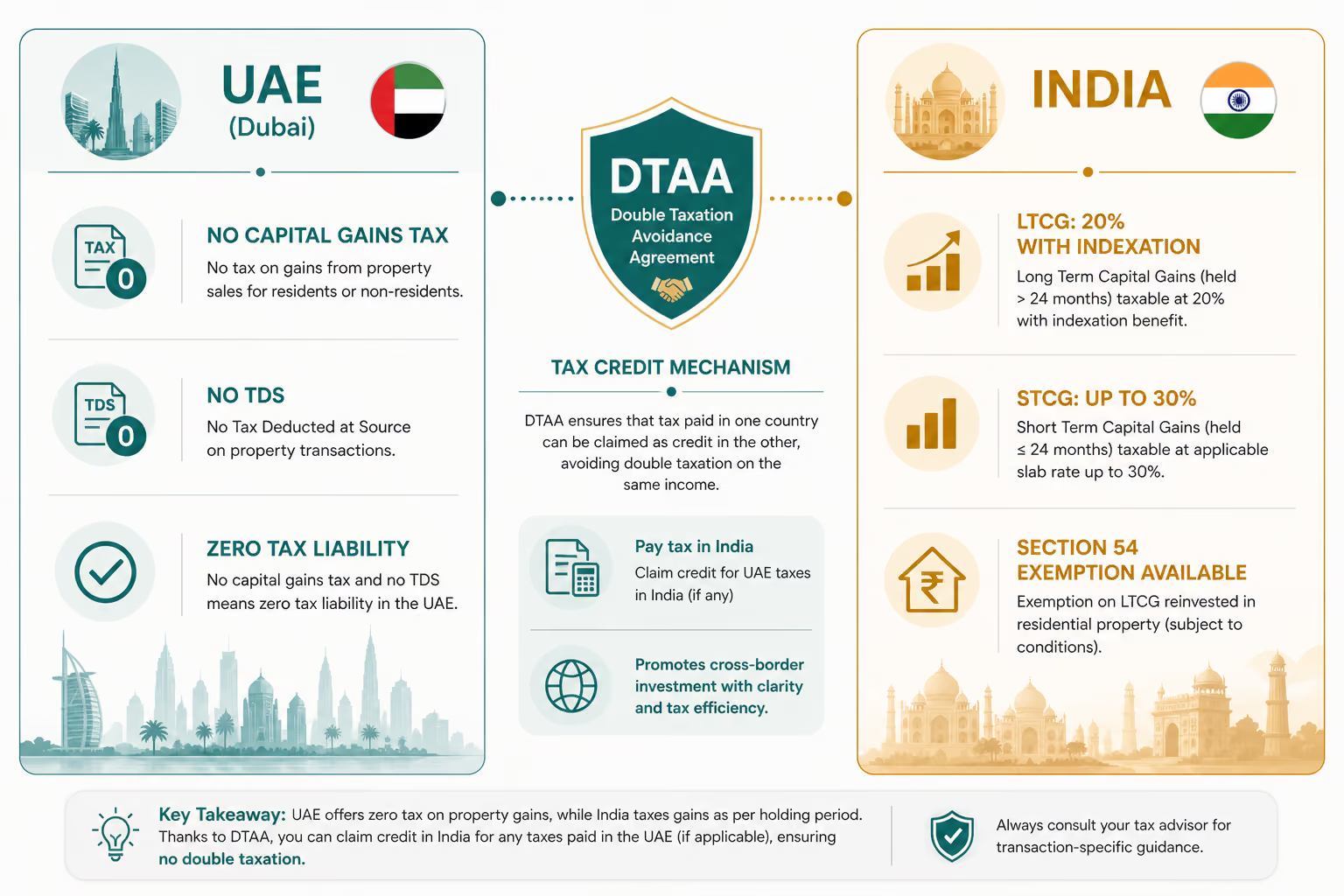

Here is the good news: the UAE does not levy any capital gains tax on property sales. There is no income tax, no wealth tax, and no inheritance tax. When you sell a property in Dubai, the entire sale proceeds are yours, minus the transaction costs (agent commission, NOC fees, DLD transfer fee).

Transaction CostTypical AmountWho PaysDLD Transfer Fee4% of sale priceSplit 50/50 (buyer/seller) or negotiableAgent Commission2% of sale priceSellerNOC FeeAED 500-5,000SellerMortgage Release (if applicable)AED 1,000-3,000SellerTrustee Office FeeAED 4,000 + VATSplit or negotiable

Full breakdown of every fee in our DLD fees and charges guide.

Tax on Dubai Property Sale: India Side

This is where it gets serious. As an NRI, your global income is not taxable in India, but capital gains from the sale of any asset are. And India considers your Dubai property an asset.

Short-Term vs Long-Term Capital Gains

Holding PeriodClassificationTax Rate (India)Less than 2 yearsShort-Term Capital Gain (STCG)Taxed at your income tax slab rate (up to 30%)2 years or moreLong-Term Capital Gain (LTCG)20% with indexation benefit (Section 112)

The 2-year threshold is critical. If you sell within 2 years of purchase, the gains are taxed at your regular slab rate, which could be as high as 30% plus cess. If you hold for 2 years or more, the rate drops to 20% with indexation, which adjusts the purchase price for inflation and can significantly reduce your taxable gain.

Indexation Benefit Explained

Indexation allows you to increase your original purchase price by the Cost Inflation Index (CII) published by the Indian government. For example, if you bought a property in 2022 for AED 1M (approximately INR 2.25 Cr at the time) and the CII has increased by 15% by 2026, your indexed cost becomes INR 2.59 Cr. This reduces the taxable gain and your tax liability.

Section 54 Exemption

If you reinvest the capital gains into a residential property in India within 2 years of sale (or 3 years for construction), you can claim exemption under Section 54 of the Income Tax Act. The exemption covers the capital gain amount, not the entire sale proceeds. This is one of the most used tax-saving strategies for NRIs selling overseas property.

DTAA: India-UAE Double Tax Avoidance

India and the UAE have a Double Taxation Avoidance Agreement. Since the UAE charges zero capital gains tax, there is no foreign tax credit to claim against your Indian liability. The DTAA prevents the same income from being taxed twice, but since the UAE does not tax it at all, India has full taxing rights.

What the DTAA does help with is preventing issues with other income types. For example, rental income from Dubai property is taxable in India, and any UAE taxes paid on that income (there are none currently, but this could change) would be creditable against Indian tax.

Repatriating Sale Proceeds to India

Getting the money from your Dubai bank account to your Indian NRE or NRO account involves FEMA compliance. Here is the step-by-step:

Step 1: Complete the Sale in Dubai

The buyer pays you through a manager's cheque or bank transfer at the DLD Trustee Office. The funds land in your UAE bank account.

Step 2: Obtain Required Documents

- Sale and Purchase Agreement (original, signed)

- Title Deed Transfer confirmation from DLD

- Bank statement showing sale proceeds received

- Original Purchase Agreement and proof of payment

- TDS Certificate (Form 16A) if TDS was deducted by the buyer in India context

- CA Certificate confirming tax compliance under FEMA

Step 3: CA Certificate for Repatriation

This is the most critical document. Your Chartered Accountant in India must issue a certificate confirming that the repatriation is FEMA-compliant, that applicable taxes have been paid or provided for, and that the amount does not exceed the original investment plus capital appreciation. The bank will not process the transfer without this certificate.

Step 4: Transfer to NRE or NRO Account

You can transfer to your NRE account (fully repatriable) or NRO account (repatriable up to USD 1 million per year under the Liberalised Remittance Scheme). For most property sales, the NRE route is preferred because there are no repatriation limits on the original investment amount.

Step 5: File Indian Tax Return

Declare the capital gains in your Indian ITR for the relevant assessment year. Pay any tax due. Keep all documentation for at least 7 years.

Common Mistakes NRIs Make When Selling

1. Not accounting for Indian tax liability before pricing

Many NRIs calculate their profit based on the Dubai sale price minus the Dubai purchase price and forget the 20% LTCG tax in India. Your actual take-home is significantly lower than the gross gain. Factor this into your asking price.

2. Missing the 2-year holding threshold

Selling at 23 months instead of 24 months can mean the difference between 20% LTCG (with indexation) and 30% STCG (without). If you are close to the 2-year mark, it almost always pays to wait.

3. Not getting the CA certificate before transferring

Your Indian bank will reject the incoming transfer if the CA certificate is not in place. Get it sorted before you initiate the transfer, not after.

4. Closing the UAE bank account too early

You need your UAE bank account active to receive the sale proceeds and to initiate the outward transfer. Do not close it until the money is safely in your Indian account.

5. Ignoring TDS obligations

If the buyer is paying from India or if the transaction is routed through Indian banking channels, TDS may apply. Consult your CA on whether advance tax or TDS provisions are triggered.

Selling Off-Plan Before Handover

If you bought off-plan and want to sell before handover (a resale assignment), the process is slightly different. You are selling your rights under the SPA, not a completed property. DLD handles this through the Oqood transfer system.

Our guide to buying property in Dubai as an Indian investor covers the off-plan purchase mechanics that are relevant to understanding resale timing and obligations.

Considering reinvesting in a new Dubai property instead of repatriating? Bond Enclave in Arjan and

Currency Conversion and Exchange Rate Impact

The exchange rate between AED and INR plays a significant role in your actual returns. When you bought the property, you converted INR to AED at one rate. When you sell and repatriate, you convert AED back to INR at a different rate. If the AED has strengthened against the INR during your holding period (which it generally has, given the AED is pegged to the USD), your INR returns are amplified beyond the property appreciation alone.

For Indian tax purposes, the RBI reference rate on the date of the sale transaction is used to calculate the INR equivalent of the sale price. The purchase price is converted using the rate on the date of purchase. This means currency gains are effectively baked into your capital gains calculation, and you will pay Indian tax on the combined property appreciation plus currency gain.

Timing your repatriation can also matter. If you have flexibility on when to transfer the funds from your UAE account to India, monitoring the AED-INR exchange rate and transferring during a favourable window can add 1-3% to your effective return. However, do not hold funds in the UAE indefinitely waiting for a better rate, as this creates FEMA compliance questions about the purpose and duration of the holding.

Key Takeaways

- Zero capital gains tax in UAE. Your tax liability is entirely in India.

- Hold for 2+ years to qualify for LTCG at 20% with indexation instead of STCG at up to 30%.

- Section 54 exemption available if you reinvest gains into Indian residential property within 2-3 years.

- CA certificate is mandatory for repatriating sale proceeds to India under FEMA.

- Factor Indian tax into your pricing. Your take-home is significantly less than the gross gain.

- Keep your UAE bank account open until all funds are successfully transferred.

Pearlshire Real Estate Development works with NRI buyers across India and the Gulf. Explore Bond Enclave and Bond Living at pearlshire.com.

Do I pay capital gains tax in UAE when selling property?

No. The UAE has zero capital gains tax. Your tax liability is only in India, based on your holding period and the applicable STCG or LTCG rates.

Can I repatriate the full sale amount to India?

Yes, subject to FEMA compliance and the CA certificate. The original investment amount is freely repatriable. Capital gains are also repatriable after paying applicable Indian taxes.

What if I bought the property with a mortgage?

You must clear the mortgage before or at the time of sale. The buyer's payment typically goes through the bank to settle the outstanding loan first, with the balance released to you.

Do I need to be physically present in Dubai to sell?

Not necessarily. You can authorise a representative via a Power of Attorney to handle the sale and DLD transfer on your behalf. The POA must be notarised and attested.

How long does repatriation take?

Once you have all documents in order (CA certificate, sale proof, bank statements), the actual transfer takes 3-5 business days. Getting the documents ready can take 2-4 weeks.

What exchange rate applies for tax calculation?

The RBI reference rate on the date of sale is used to convert the AED sale price to INR for Indian tax purposes. Currency fluctuations between purchase and sale dates also affect your calculated gain.