NRI Guide to Buying Property in Dubai 2026: Tax Rules, FEMA Compliance & LRS Limits Explained

NRIs can buy freehold property in Dubai with full ownership rights. The LRS limit is USD 250,000 per person per year through authorized dealer banks. Rental income is taxable in India under Income from Other Sources. Non-disclosure of Dubai property in Schedule FA triggers 30% tax plus 90% penalty under the Black Money Act.

Indian nationals account for over 58% of all Dubai real estate transactions. That's not a niche market—that's the market. But buying Dubai property as an NRI isn't just about finding the right apartment or villa. There's a compliance layer that most Dubai real estate guides completely overlook: FEMA regulations, LRS limits, Indian tax reporting, and the implications of the Black Money Act.

The good news? It's manageable. With the right approach and proper documentation, buying Dubai property as an NRI is straightforward. The bad news? Skip the compliance steps, and you're looking at serious penalties from the Indian tax authorities. This guide walks you through every step—from FEMA remittance to filing Schedule FA in your ITR.

Can NRIs Buy Property in Dubai? Yes, and Here's How

The short answer: Yes. NRIs have exactly the same property ownership rights as UAE nationals in designated freehold areas across Dubai.

Here's what you need to know:

Full Freehold OwnershipIn freehold zones—which cover most of Dubai's premium developments—foreign nationals including NRIs own 100% of the property with no restrictions. You're not leasing. You're not bound by a timeframe. This is actual ownership that you can hold indefinitely, rent out, sell, or leave in your will.

No Residency RequirementYou don't need to be a Dubai resident, a UAE resident, or even have a visa to purchase property. You can buy from India, from any UAE emirate, or from anywhere else. The only requirement is capital and a valid passport.

Same Rights Across Property TypesWhether you're buying an apartment in a high-rise, a villa in a gated community, a townhouse, or a plot of land, the ownership structure is identical. All freehold properties in designated areas carry the same legal standing.

Why Dubai's System Works for Foreign InvestorsDubai's real estate framework is built on transparency. The Dubai Land Department (DLD) maintains a clear registry. Transactions are regulated. There's no ambiguity about ownership or title. For NRIs comparing Dubai to property investments in other jurisdictions, this regulatory clarity is a significant advantage.

Recent data shows that Indian buyers consistently represent between 55-60% of Dubai's transaction volume, making them the single largest buyer demographic in the Emirates. This dominance isn't accidental—it reflects both the strength of the India-UAE relationship and the practical appeal of Dubai's legal framework for Indian wealth.

FEMA Rules for NRIs Buying Property in Dubai (2026 Update)

FEMA—the Foreign Exchange Management Act—is India's framework governing cross-border currency transactions. If you're remitting rupees to dirhams to buy Dubai property, FEMA applies to you.

What NRIs Are Allowed to Do

Under FEMA, NRIs can invest in overseas property directly from NRE accounts (Non-Resident External accounts) or NRO accounts (Non-Resident Ordinary accounts). This isn't a gray area. It's explicitly permitted. India wants NRIs to invest in foreign real estate.

The vehicle for this is the Liberalised Remittance Scheme (LRS), introduced by the Reserve Bank of India.

The LRS Limit: USD 250,000 Per Person, Per Year

Under LRS, each NRI can remit up to USD 250,000 per calendar year for overseas property investment. This limit applies to each individual, not per family.

What does this mean practically?

- Single buyer: You can remit up to USD 250K in 2026 for your Dubai property purchase.

- Married couple (both NRI): You can remit USD 500K combined—USD 250K from each spouse's account.

- Going beyond USD 250K: If your property costs more than USD 250K, you can wait until the next calendar year and remit an additional USD 250K. Alternatively, you can explore alternative financing structures (discussed below).

The Remittance Process: You Must Use an Authorized Dealer Bank

You cannot transfer funds via unofficial channels. You must route your remittance through an authorized dealer (AD) bank in India. Common examples include HDFC Bank, ICICI Bank, Axis Bank, and Kotak Mahindra Bank. These banks process LRS remittances directly to your Dubai account.

The process is:

- Inform your AD bank that you're remitting under LRS for property investment.

- Provide required documentation (see below).

- The bank facilitates the INR-to-USD conversion at current RBI rates.

- Funds are transferred to your Dubai bank account.

- The bank files LRS declaration with RBI.

Documentation Required for LRS Remittance

Have these documents ready before approaching your bank:

- PAN Card: Your Permanent Account Number (mandatory).

- Passport: Copy of your NRI passport.

- Bank Statements: Recent 6 months of statements from your NRE/NRO account.

- Form 15CA: Tax compliance certificate issued by a Chartered Accountant (required for remittances above INR 50,000).

- Form 15CB: Alternative to 15CA if your income is below ITR filing threshold (rarely used for property investment).

- ITR Copy: Recent income tax return (last 1-2 years).

- Property Documentation: Copy of SPA (Sales Purchase Agreement) or property agreement from Dubai developer/seller.

The Form 15CA is the step many NRIs miss. It's a certification from a CA that the remittance is not for prohibited purposes. It takes a few days to obtain, so plan ahead.

Joint Purchases and Dual Accounts

If you and your spouse are both buying the property jointly, each spouse has a separate USD 250K limit. This allows a couple to remit USD 500K in a single year.

However, if only one spouse has earned income or holds an NRE account, only that spouse can remit under LRS. The non-earning spouse cannot use LRS unless they have their own NRE account with documented income or savings.

Alternative Structures for Larger Investments

Some NRIs with property budgets exceeding USD 500K use corporate structures—purchasing through a UAE company registered in the free zones. This is a different FEMA framework and allows larger remittances, but it involves additional compliance, corporate taxation, and structuring costs. This route is typically used only for commercial properties or very large residential investments.

For standard residential property purchases, LRS is the simplest path.

Indian Tax Obligations When You Own Dubai Property

Here's the reality that often surprises NRIs: Dubai doesn't tax your property income. But India does. Understanding both sides is crucial.

Dubai Side: Zero Tax

Let's be clear—Dubai property is incredibly tax-efficient from a cash flow perspective.

- No capital gains tax on property sale (regardless of profit).

- No rental income tax on lease payments you collect.

- No annual property tax on ownership.

The only compulsory fee is the DLD transfer fee (also called registration fee), which is 4% of the property value. This is paid at purchase (if buying from an owner) and again at sale (split between buyer and seller). It's a one-time transaction fee, not an ongoing tax.

This tax neutrality on property income is a major reason NRIs prefer Dubai over many other overseas property markets.

India Side: Reporting is Non-Negotiable

But the moment you, as an Indian resident or NRI, own property abroad, India's tax authority (Income Tax Department) wants to know about it. And they want documentation of income generated.

Rental Income

If you're renting out your Dubai property, the rental income is taxable in India under "Income from Other Sources." It doesn't matter that you paid no tax in Dubai. India taxes it at your applicable income tax slab rate (up to 30% for top earners, plus applicable surcharge and cess).

You must:- Report the annual rental income in your ITR.- Deduct mortgage interest (if applicable) and maintenance costs to arrive at net taxable rental income.- Pay income tax on the net amount.

Capital Gains on Sale

When you sell your Dubai property, the gain (sale price minus original cost) is taxable in India.

- Short-term capital gain (held < 24 months): Taxed at your applicable income tax slab rate (up to 30%).

- Long-term capital gain (held ≥ 24 months): Taxed at 20% with indexation benefit (which reduces the taxable gain by accounting for inflation), or 12.5% under the new tax regime without indexation.

The indexation benefit means your original purchase cost is adjusted upward for inflation, reducing your taxable capital gain. This is a significant advantage for long-term property holding.

Double Tax Avoidance Agreement (DTAA)

India and the UAE have a Double Tax Avoidance Agreement. Here's what it means: Since Dubai imposes zero tax on property income and capital gains, India gets full taxing rights. You won't pay tax in both places. But you will pay tax in India.

Schedule FA: The Critical Compliance Step

This is where many NRIs make a catastrophic mistake.

All foreign assets—including Dubai property—must be disclosed in Schedule FA (Schedule for Foreign Assets) of your Indian income tax return. Schedule FA requires you to list:

- Asset location: Dubai, UAE

- Nature of asset: Residential property / Apartment / Villa

- Estimated value: Fair market value of the property

- Rental income during the year: If applicable

- Capital gains on sale: If you sold the property during the year

Even if your property generates zero rental income and you haven't sold it, you must still file Schedule FA listing the property and its estimated value.

Failure to disclose is not a minor compliance miss. It falls under India's Benami Transactions (Prohibition) Amendment Act and the Schedule FA disclosure requirements, with penalties under the Black Money Act.

Penalties for Non-Disclosure

If you own Dubai property and don't disclose it in Schedule FA:

- 30% tax on the value of undisclosed foreign assets.

- 90% penalty on top of the tax.

- This is not negotiable or partial. The tax authority can impose the full 30% + 90% penalty structure.

For an NRI with a USD 400K property in Dubai, non-disclosure could result in penalties exceeding INR 25 lakhs—far exceeding the tax liability you would have faced with proper disclosure.

Disclosure is non-negotiable.

NRI Buying Property in Dubai: Step-by-Step Process

Here's the exact path from decision to ownership:

Step 1: Property Selection and ResearchChoose your property and developer carefully. Research the location (rental yield, appreciation potential, infrastructure), the developer's track record, and whether it qualifies for the Golden Visa (AED 2M minimum if that's your goal).

Step 2: Arrange Finances and LRS RemittanceCalculate the total cost (property price + DLD fees + legal fees). If it exceeds your annual LRS limit, plan for multi-year remittance or alternative structuring. Apply for Form 15CA, inform your AD bank of your LRS remittance, and initiate the fund transfer to your Dubai bank account.

Step 3: Sign the Sales Purchase Agreement (SPA)Once funds are in your Dubai account, you and the developer/seller sign the SPA. This document outlines payment terms, handover date, and conditions. Ensure you have independent legal review.

Step 4: Pay the Booking DepositTypically 10-20% of the property price is paid as a booking deposit and held in an escrow account.

Step 5: DLD Registration or Off-Plan Oqood- For off-plan properties: The developer applies for an Oqood (preliminary sales agreement) with the DLD, registering your purchase.- For ready properties: Title transfer is registered directly with the DLD.

Both processes are fast (1-2 weeks) and provide legal protection.

Step 6: Complete Payment ScheduleFor off-plan: Payment is linked to construction milestones (foundation, structure, finishing, handover). For ready properties: Balance payment is due upon transfer or shortly after.

Step 7: Golden Visa Application (If Eligible)If the property value is AED 2M or above, you're eligible for a Golden Visa. After completing payment and registration, you can apply for a 10-year renewable visa through the General Directorate of Residency and Foreigners Affairs (GDRFA) or ICP (Immigration and Citizenship Program). This process is handled with the help of a local agent or the developer's setup assistance.

Step 8: Property Management SetupIf you intend to rent out the property, arrange property management (leasing, tenant screening, maintenance, collection). Many international property management firms in Dubai specialize in managing absentee NRI owners.

Step 9: Report in Indian ITRIn your annual Indian income tax return:- Disclose the property in Schedule FA with estimated value.- Report any rental income under "Income from Other Sources."- If you sold the property during the year, declare capital gains.- Have your CA file the ITR with proper documentation.

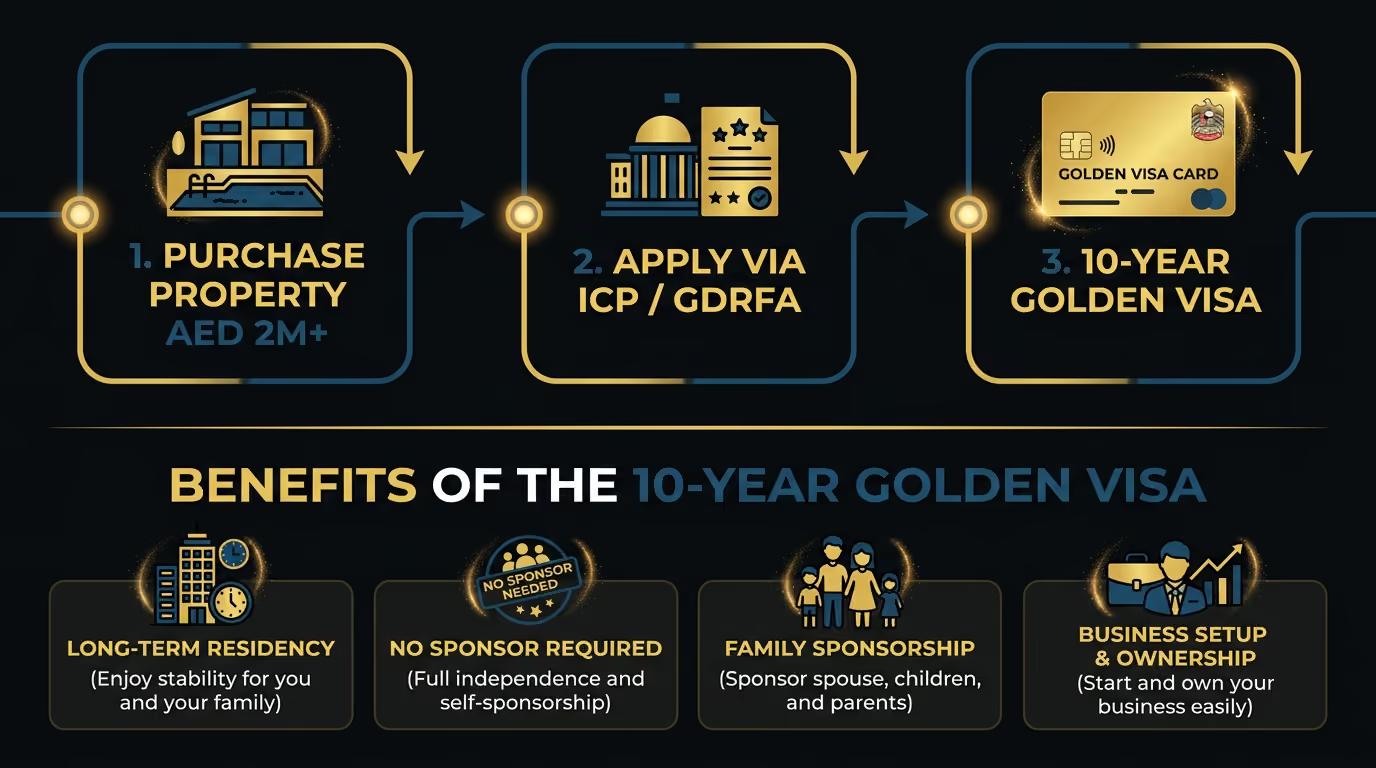

Golden Visa Through Property for NRIs: The AED 2M Pathway

The UAE Golden Visa is one of the most attractive residency benefits for NRI property investors.

Eligibility

To qualify for a Golden Visa through property:

- Minimum property value: AED 2,000,000 (approximately USD 545,000).

- Property type: Residential property (apartments, villas, townhouses in freehold areas).

- Single or multiple properties: You can combine multiple properties to reach the AED 2M threshold (e.g., two AED 1M properties = AED 2M qualifying).

- Off-plan eligible: Yes. Even properties under construction qualify if the total value meets the threshold.

Visa Details

- Duration: 10 years, renewable.

- Family sponsorship: Your spouse and children can be sponsored under the same visa.

- No mandatory employment: You don't need a job offer or employer sponsorship.

- No exit requirement: You're not required to live in the UAE permanently, though the visa allows you to.

Why This Matters for NRIs

The Golden Visa is genuinely transformative for NRI families considering Dubai. It offers:

- Long-term residency flexibility: Send your child to school in Dubai. Use it as a base for business travel across the Middle East. Maintain an international presence without visa run-around.

- Investment security: Your legal residency status is independent of employment, reducing relocation risk.

- Family planning: Sponsor your spouse and children for 10 years at a time with minimal bureaucracy.

- Tax residency planning: The UAE has no personal income tax. For some NRI family situations, becoming a UAE resident under the Golden Visa can have tax planning implications in conjunction with Indian tax residency rules.

How It Works

- You purchase a property worth AED 2M+ in a qualifying freehold area.

- Complete the purchase and obtain the title deed from the DLD.

- Apply for the Golden Visa through GDRFA or an authorized agent.

- Processing takes 4-6 weeks typically.

- Upon approval, your family receives 10-year residence visas.

Pearlshire's Advantage

Both Bond Enclave and Bond Living in Arjan offer properties within the Golden Visa-eligible bracket. As an NRI buyer, you get developer support navigating both the property purchase and the visa application process.

India Budget 2026: What Changed for NRI Property Investors

The 2026 Indian Union Budget brought several changes relevant to NRI property investors:

Expanded Remittance Clarity

The RBI and Ministry of Finance have clarified that the LRS limit remains USD 250,000 per person per year with no indication of reduction. The government has actually encouraged NRI overseas investment as part of broader capital management policy.

Simplified ITR Filing for NRIs

The income tax filing process for NRIs reporting foreign assets has been streamlined with clearer Schedule FA guidance and online tools to calculate foreign asset values in INR.

Reduced TCS on Property Remittances

Tax Collected at Source (TCS) on overseas remittances for real estate has been rationalized in certain cases, reducing the upfront cash requirement for some NRIs during fund transfer.

Capital Gains Tax Regime Adjustments

The new personal income tax regime (optional, introduced in 2023) now includes clarity on long-term capital gains taxation, which affects property sale planning for NRIs.

Direction of Policy

The overarching message from the 2026 budget is clear: India is making it easier for NRIs to invest overseas, not harder. The government views NRI real estate investment as a positive capital flow, and policy is trending toward simplification of compliance and reduction of administrative burden.

Dubai vs India Property Investment: Why NRIs Choose Dubai

For context, here's how Dubai and India property investments compare across key metrics:

The numbers tell the story: Dubai property offers superior rental yield, zero capital gains taxation, and stronger legal frameworks for property owners. For an NRI comparing property investment options, the financial advantage of Dubai is substantial.

Common Mistakes NRIs Make When Buying Dubai Property

Mistake 1: Not Reporting in Schedule FA

This is the most critical error. Some NRIs believe that since they paid no tax in Dubai, there's nothing to report to India. This is wrong and dangerous. Non-disclosure triggers Black Money Act penalties.

Mistake 2: Exceeding LRS Limit Without Planning

Buying a USD 400K property with only USD 250K LRS available per year requires multi-year planning or alternative structures. Some NRIs use informal hawala channels to source additional funds—this is illegal and detectable.

Mistake 3: Using Non-Authorized Channels for Remittance

Hawala, underground brokers, and informal money transfer services are not only illegal under FEMA but also create an audit trail that Indian tax authorities can trace. Always remit through your AD bank.

Mistake 4: Buying in Leasehold Rather Than Freehold Areas

Some developers offer properties in leasehold areas with 99-year or 125-year leases. While valid, these are not pure freehold ownership and have different resale dynamics. Ensure you understand whether your property is freehold or leasehold.

Mistake 5: Ignoring Service Charges in ROI Calculations

Dubai properties carry annual service charges (AED 20-50 per sqft depending on amenities and location). Many NRIs calculate rental yield without accounting for these ongoing costs, inflating expected returns.

Mistake 6: Proceeding Without Proper Legal Review

Never sign an SPA without having a local Dubai real estate lawyer review it. The legal framework is fair, but the document details matter. A lawyer protects you against unforeseen conditions.

Mistake 7: Not Setting Up Property Management

Absentee NRI owners who try to self-manage from India face tenant communication challenges, rental collection delays, and maintenance issues. Professional property management costs 5-10% of rental income but ensures smooth operations.

Frequently Asked Questions

Q1: Can an NRI buy property in Dubai directly from India?

Yes, absolutely. You don't need to be physically present in Dubai to purchase property. You can sign documents electronically or through power of attorney. Most of the process is paperwork-based. However, it's recommended to visit before finalizing to see the property and understand the area.

Q2: What is the LRS limit for buying property in Dubai in 2026?

USD 250,000 per person per calendar year. If you're married (both NRI), you and your spouse can remit up to USD 500,000 combined in a single year. This limit resets on January 1st of each calendar year.

Q3: Do NRIs pay tax in India on Dubai rental income?

Yes. Rental income from Dubai property must be reported in your Indian ITR under "Income from Other Sources" and is taxed at your applicable income tax slab rate. You can deduct expenses like mortgage interest and maintenance to reduce taxable income.

Q4: Is Dubai property investment eligible for the Golden Visa for Indian citizens?

Yes, if the property value is AED 2,000,000 or above. You can apply for a 10-year renewable Golden Visa that allows you, your spouse, and your children residency in the UAE. Off-plan properties also qualify.

Q5: What happens if I don't declare Dubai property in my Indian tax return?

You face severe penalties under the Black Money Act: 30% tax on the value of the undisclosed asset plus 90% penalty. For a USD 400K property, this could exceed INR 25 lakhs. Additionally, the income tax authority can reopen your returns for up to 10 years. Declaration is non-negotiable.

Ready to Invest in Dubai as an NRI?

Indian buyers are the backbone of Dubai's property market, and at Pearlshire Development, we understand the NRI journey—from LRS remittance planning to Golden Visa applications to Indian tax compliance.

Bond Enclave and Bond Living in Arjan are specifically designed for sophisticated investors who understand Dubai's market and regulatory environment. Both projects offer:

- Golden Visa-qualifying properties (AED 2M+ units available)

- Strong rental yields (7-9% range)

- Developer support navigating NRI compliance

- Off-plan pricing with flexible payment terms

- Prime location in one of Dubai's highest-growth emerging communities

Whether you're looking for a primary residence, an investment property, or a visa-backed base for your family, our team guides you through every step—including coordinating with your Indian CA and legal advisors.

Explore Bond Enclave | Explore Bond Living

Important Note

This guide is for informational purposes and reflects the tax and regulatory environment as of March 2026. FEMA rules, LRS limits, tax regimes, and visa policies are subject to change. Always consult with a qualified Indian Chartered Accountant familiar with NRI taxation and a local Dubai real estate lawyer before making any property investment decision. Your specific situation may have unique implications not covered in this general guide.

Internal Link Suggestions for Blog Navigation:- [Can Indians Buy Property in Dubai?]- [Golden Visa Property Eligibility in UAE]- [Can Foreigners Buy Property in Dubai?]- [UAE Mortgage Guide for NRIs]- [Arjan Investment Opportunities in Dubai]- [Off-Plan vs Ready Property: Which is Right for You?]- [Sharia-Compliant Banking Guide for NRI Investors]